Why Commercial Property Insurance Costs Are Increasing Across Australia

Commercial property insurance costs across Australia have risen significantly over recent years, leaving many business owners, landlords, strata owners, and commercial property investors questioning why premiums continue increasing. From rising rebuilding costs and natural disasters to stricter insurer underwriting and underinsurance concerns, the commercial property insurance market has become far more complex.

At Global Insurance Solutions, we work with businesses Australia-wide to help review commercial property insurance policies, identify coverage gaps, and navigate increasingly difficult insurance conditions. Whether you own warehouses, retail centres, offices, factories, mixed-use properties, or strata buildings, understanding why insurance costs are surging has become critical for protecting your assets and business continuity.

According to the Insurance Council of Australia, insured losses from extreme weather events have exceeded billions of dollars over recent years, significantly impacting insurer pricing models and risk appetite across commercial property sectors in Australia.

Source: https://insurancecouncil.com.au/resource/catastrophe-data/

The Australian Bureau of Statistics has also reported ongoing increases in construction and building replacement costs, contributing heavily to higher commercial property insurance premiums.

Source: https://www.abs.gov.au/statistics/economy/price-indexes-and-inflation

What is Commercial Property Insurance?

Commercial property insurance helps protect businesses and property owners against physical loss or damage to commercial buildings and associated assets caused by insured events.

An insurance for commercial property policy may help cover:

- Commercial buildings

- Fixtures and fittings

- Plant and equipment

- Glass and signage

- Loss of rent

- Business interruption

- Accidental damage

- Storm and water damage

- Fire and smoke damage

- Theft and vandalism

Commercial property insurance coverage can vary significantly depending on policy wording, insurer appetite, location, occupancy, and risk profile.

Businesses should never assume all risks are automatically covered.

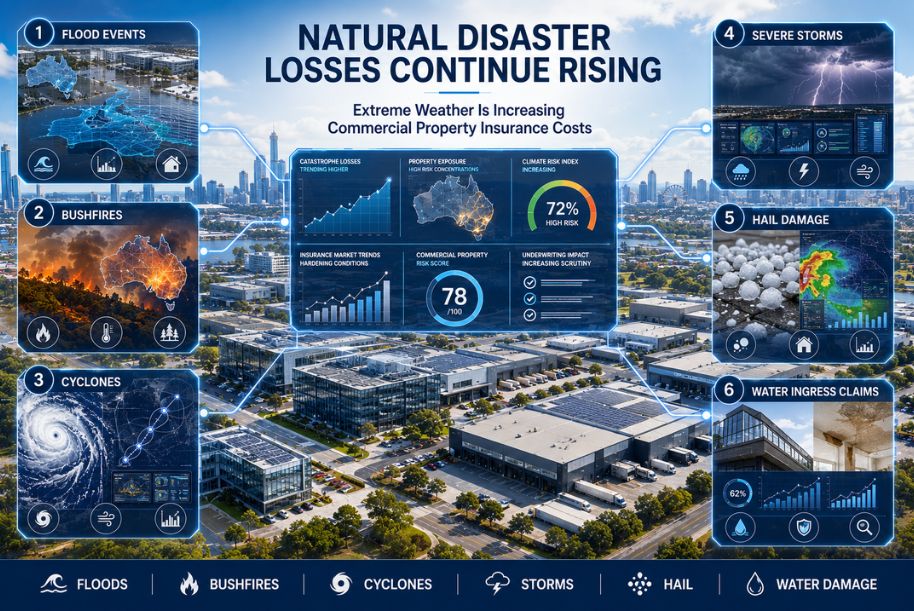

Natural Disaster Losses Continue Rising

One of the biggest reasons commercial property insurance costs are increasing is the growing frequency and severity of natural disasters across Australia.

Insurers are now dealing with:

- Flood events

- Bushfires

- Cyclones

- Severe storms

- Hail damage

- Water ingress claims

The Insurance Council of Australia has repeatedly highlighted the growing financial impact of catastrophe events on insurers and policyholders.

Source: https://insurancecouncil.com.au/resource/catastrophe-insurance-data/

Many insurers have responded by:

- Increasing premiums

- Raising excesses

- Reducing coverage

- Tightening underwriting conditions

- Limiting flood cover in high-risk areas

Properties located in flood-prone or catastrophe-exposed regions are often seeing the most significant increases.

Rebuilding Costs Have Increased Dramatically

Commercial building insurance costs are also rising because rebuilding costs have surged across Australia.

Insurers calculate premiums partly based on replacement value and reinstatement costs. As construction costs increase, insured values must also increase.

Rising costs include:

- Labour shortages

- Construction material inflation

- Supply chain delays

- Increased contractor demand

- Engineering and compliance costs

The Australian Bureau of Statistics reported ongoing increases in construction input costs following inflationary pressures across the building industry.

Many businesses are now discovering their properties may be underinsured.

Underinsurance Is Becoming a Major Problem

Underinsurance risks are becoming one of the largest concerns within commercial property insurance Australia-wide.

Many property owners still rely on outdated insured values that no longer reflect true rebuilding costs.

This creates major exposure during claims.

If sums insured are inaccurate, businesses may face:

- Reduced claim settlements

- Co-insurance penalties

- Delayed rebuilding

- Cash flow pressure

- Significant out-of-pocket expenses

Underinsurance has become increasingly common following rapid increases in building costs and inflation.

Businesses should regularly review:

- Building replacement values

- Plant and equipment values

- Tenant improvements

- Professional fees

- Demolition costs

- Debris removal costs

Insurers Are Becoming More Selective

Commercial property insurers are becoming far more cautious about the risks they insure.

Many insurers are reassessing exposure to:

- Older buildings

- High-risk occupancies

- Manufacturing facilities

- Warehouses

- Food processing businesses

- Recycling operations

- Properties in flood zones

- Vacant buildings

This reduced insurer appetite often results in:

- Higher premiums

- More exclusions

- Reduced competition

- Higher deductibles

- Stricter risk management requirements

Businesses with poor claims history or inadequate maintenance are often seeing sharper premium increases.

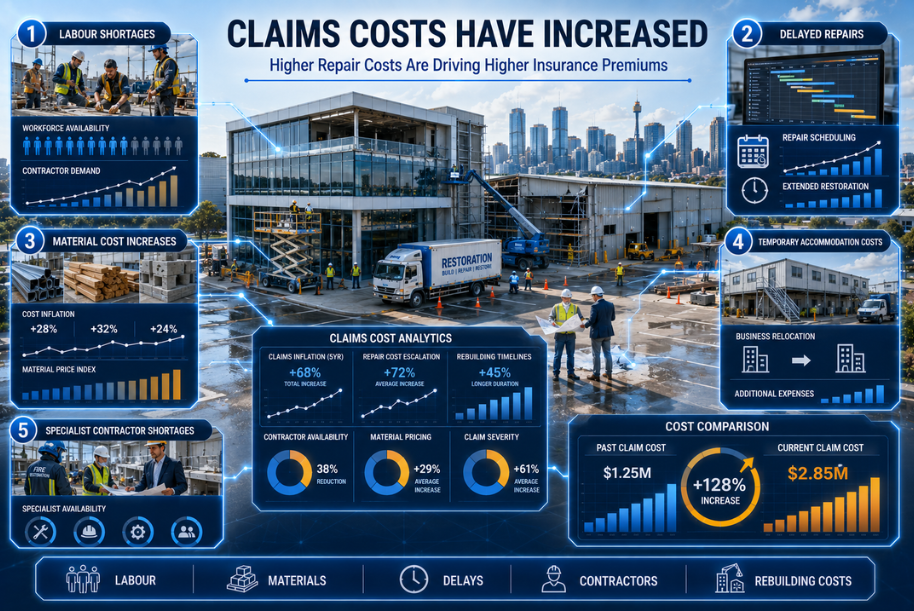

Claims Costs Have Increased

Insurance claims are becoming significantly more expensive to settle.

Even relatively straightforward commercial property damage insurance claims now involve higher costs due to:

- Labour shortages

- Delayed repairs

- Material cost increases

- Temporary accommodation costs

- Specialist contractor shortages

For example, a commercial fire insurance claim today may cost substantially more than a similar claim several years ago because rebuilding timelines and material pricing have changed dramatically.

This directly impacts how insurers calculate commercial property insurance rates.

Business Interruption Claims Are More Complex

Business interruption commercial property insurance has become another major factor influencing premium increases.

Following natural disasters, supply chain disruptions, and operational shutdowns, insurers are seeing larger and longer business interruption claims.

Businesses are now more dependent on:

- Technology

- Suppliers

- Logistics networks

- Critical infrastructure

- Digital systems

Recovery periods after major property losses are also becoming longer.

As a result, insurers are carefully assessing:

- Indemnity periods

- Gross profit exposure

- Dependency risks

- Supply chain vulnerabilities

- Revenue concentration

Does Commercial Property Insurance Cover Fire, Flood & Theft?

Does Commercial Property Insurance Cover Fire?

In most cases, yes.

Fire insurance for commercial property is one of the core insured events typically included under commercial property insurance policies.

However, businesses should still carefully review:

- Policy exclusions

- Maintenance obligations

- Electrical compliance requirements

- Hazardous occupancy conditions

Does Commercial Property Insurance Cover Flood Damage?

Flood insurance commercial property cover varies significantly between insurers.

Some policies include flood cover automatically, while others may:

- Exclude flood entirely

- Apply sub-limits

- Impose higher excesses

- Require additional underwriting

Flood definitions within policy wording are extremely important.

Does Commercial Property Insurance Cover Theft?

Theft covered under commercial property insurance often depends on:

- Security protections

- Alarm systems

- Forced entry evidence

- Occupancy conditions

Certain high-risk industries may face tighter theft conditions.

Does Commercial Property Insurance Cover Roof Leaks?

Roof leak insurance claim commercial property scenarios depend heavily on causation.

Storm-related sudden damage may be covered.

However, gradual deterioration, poor maintenance, rust, corrosion, or pre-existing defects are commonly excluded.

Does Commercial Property Insurance Cover Vandalism?

Many commercial property insurance policies include vandalism and malicious damage cover.

Vacant properties may face stricter conditions or exclusions.

What Factors Influence Commercial Property Insurance Costs?

Several factors affect how commercial property insurance premiums are calculated.

Building Construction Type

Insurers assess:

- Building age

- Construction materials

- Fire resistance

- Roof type

- Structural integrity

Older buildings generally attract higher premiums.

Property Location

Location plays a significant role.

Insurers assess exposure to:

- Flood

- Bushfire

- Cyclone

- Crime

- Storm activity

Occupancy Type

Certain occupancies are considered higher risk, including:

- Manufacturing

- Warehousing

- Hospitality

- Fuel operations

- Recycling

- Chemical storage

Claims History

Previous claims can significantly influence insurer appetite and pricing.

Risk Management Measures

Strong risk management may help reduce premiums, including:

- Fire protection systems

- CCTV

- Alarm systems

- Maintenance programs

- Emergency response plans

Is Commercial Property Insurance Mandatory in Australia?

Commercial property insurance is generally not legally mandatory in Australia.

However, lenders, lease agreements, strata obligations, and contractual requirements often make insurance effectively essential.

Commercial landlords commonly require tenants to maintain certain forms of insurance.

Similarly, financiers typically require building insurance before approving loans.

Common Commercial Property Insurance Claim Mistakes

Many businesses only discover policy gaps after a claim occurs.

Common mistakes include:

Inadequate Sums Insured

Underestimating replacement costs remains one of the biggest causes of claim shortfalls.

Failing to Understand Exclusions

Many businesses assume policies cover all damage scenarios.

Policy wording matters significantly.

Delayed Maintenance

Poor maintenance can contribute to claim denials involving:

- Roof leaks

- Water ingress

- Structural deterioration

Incorrect Occupancy Disclosure

Businesses must accurately disclose activities and occupancy details to insurers.

Incorrect disclosures can impact claims.

You can read the full blog on common insurance claim pitfalls for property owners.

How Businesses Can Better Manage Rising Insurance Costs

Although premiums are increasing, businesses can still take proactive steps to improve their insurance position.

Review Insurance Annually

Businesses should regularly review:

- Sums insured

- Property valuations

- Business interruption exposure

- Policy wording

- New operational risks

Improve Risk Management

Strong risk controls may improve insurer confidence.

Work With an Experienced Broker

A building insurance broker can help businesses:

- Compare insurers

- Negotiate terms

- Identify coverage gaps

- Review exclusions

- Structure policies correctly

- Assist with claims

At Global Insurance Solutions, we work with businesses Australia-wide to help navigate changing insurer appetites and rising commercial property insurance costs.

We understand the challenges businesses face when trying to balance affordability with adequate protection.

Why Commercial Property Insurance Reviews Matter More Than Ever

The Australian insurance market continues to evolve rapidly.

Businesses are now facing:

- Rising rebuilding costs

- More severe weather events

- Increasing insurer scrutiny

- Inflationary pressure

- Complex policy wording

- Higher excesses

Commercial property insurance should no longer be treated as a once-a-year renewal exercise.

Regular reviews may help businesses identify potential underinsurance risks, outdated insured values, and policy gaps before a major loss occurs.

At Global Insurance Solutions, we help businesses across Australia review commercial property insurance policies and navigate increasingly complex risk environments with practical insurance advice and claims-focused support.

Also Read: Landlord Insurance vs Building Insurance

Frequently Asked Questions

Q1. What does commercial property insurance cover?

Ans 1. Commercial property insurance generally helps cover buildings, contents, equipment, and business assets against insured events such as fire, storms, theft, vandalism, and accidental damage.

Q2. Does commercial property insurance cover flood damage?

Ans 2. Some policies include flood cover, while others may exclude it or apply specific conditions and higher excesses.

Q3. Does commercial property insurance cover fire?

Ans 3. Yes. Fire is one of the most common insured events covered under commercial property insurance policies in Australia.

Q4. Does commercial property insurance cover roof leaks?

Ans 4. It depends on the cause. Sudden storm-related roof damage may be covered, while gradual deterioration or poor maintenance is commonly excluded.

Q5. Does commercial property insurance cover vandalism?

Ans 5. Many policies include vandalism and malicious damage cover, although certain conditions may apply.

Q6. Is theft covered under commercial property insurance?

Ans 6. Many commercial property insurance policies provide cover for theft and burglary, subject to security requirements and policy wording.

Q7. How much does commercial property insurance cost in Australia?

Ans 7. Commercial property insurance costs vary depending on location, building type, occupancy, flood exposure, replacement value, claims history, and risk profile.

Q8. Is commercial property insurance compulsory in Australia?

Ans 8. Commercial property insurance is generally not legally mandatory, although lenders and lease agreements often require it.

Q9. What factors affect commercial property insurance premiums?

Ans 9. Premiums are influenced by building construction, location, catastrophe exposure, occupancy, security protections, claims history, and replacement costs.

Q10. Who is responsible for building insurance in commercial property?

Ans 10. In many cases, the property owner or landlord arranges building insurance, although lease agreements may allocate certain responsibilities differently.

Important notice

This article is of a general nature only and does not take into account your specific objectives, financial situation or needs. It is also not financial advice, nor complete, so please discuss the full details with your insurance broker as to whether these types of insurance are appropriate for you. Deductibles, exclusions and limits apply. You should consider any relevant Target Market Determination and Product Disclosure Statement in deciding whether to buy or renew these types of insurance. Various insurers issue these types of insurance and cover can differ between insurers.

This article provides information rather than financial product or other advice. The content of this article, including any information contained in it, has been prepared without taking into account your objectives, financial situation or needs. You should consider the appropriateness of the information, taking these matters into account, before you act on any information. In particular, you should review the product disclosure statement for any product that the information relates to it before acquiring the product.

Information is current as at the date the article is written as specified within it but is subject to change. Global Insurance Solutions Pty Ltd make no representation as to the accuracy or completeness of the information. Various third parties have contributed to the production of this content. All information is subject to copyright and may not be reproduced without the prior written consent of Global Insurance Solutions Pty Ltd.

Risk Advisor, Insurance Broker & Director

With around 15 years in insurance, Yuvi Singh is a passionate Risk Advisor, Director, and Insurance Broker at Global Insurance Solutions. Backed by a Commerce degree and ANZIIF diploma, Yuvi leads a team servicing SMEs across industries like manufacturing, logistics, fuel, IT, and more. At GIS, clients benefit from tailored, transparent advice, access to 150+ insurers, and end-to-end risk solutions. Recognised as a 2022 Insurance Magazine Rising Star and 2024 Top Insurance Broker by Insurance Business Australia, Yuvi delivers flexible, effective outcomes with integrity and innovation.