Australian businesses continue to navigate a challenging economic environment shaped by changing interest rates, inflationary pressures and rising operating expenses. Whether you’re a small business owner, property investor, manufacturer, retailer or professional services provider, the impact of interest rate rises Australia has experienced over recent years continues to influence borrowing costs, investment decisions and overall profitability.

While many businesses focus on managing loans, financing arrangements and cash reserves during periods of economic change, one critical area is often overlooked: business insurance Australia.

As business insurance costs continue to rise and insurers reassess risk across multiple industries, now may be the ideal time to undertake a comprehensive business insurance review. For many organisations, reviewing insurance arrangements can help identify coverage gaps, reduce the risk of underinsurance and ensure policies continue to align with current business operations.

At Global Insurance Solutions, we are seeing more businesses across Australia proactively review their insurance portfolios as part of broader financial planning and risk management strategies.

Why Rising Interest Rates Should Trigger a Business Insurance Review

The impact of rising interest rates on business extends well beyond lending costs.

Higher interest rates often influence:

- Property values

- Construction costs

- Equipment financing expenses

- Supply chain costs

- Labour expenses

- Business expansion plans

- Cash reserves and liquidity

As businesses adjust their operations to respond to changing economic conditions, insurance arrangements can quickly become outdated.

A professional business insurance review allows businesses to assess whether their insurance policies still reflect current exposures, asset values and operational risks.

Many businesses review budgets annually but fail to review their business insurance with the same level of scrutiny.

An effective review can help ensure:

- Policies remain relevant

- Coverage limits remain adequate

- Premiums remain competitive

- New business risks are identified

- Existing policies continue to provide appropriate protection

For businesses operating in today’s environment, a proactive approach to insurance can form an important part of overall business risk management strategies in Australia.

How Changing Economic Conditions Can Impact Business Insurance?

Australia’s economic landscape continues to evolve.

Factors influencing businesses include:

- Inflation

- Wage growth

- Labour shortages

- Supply chain disruptions

- Increased borrowing costs

- Rising energy prices

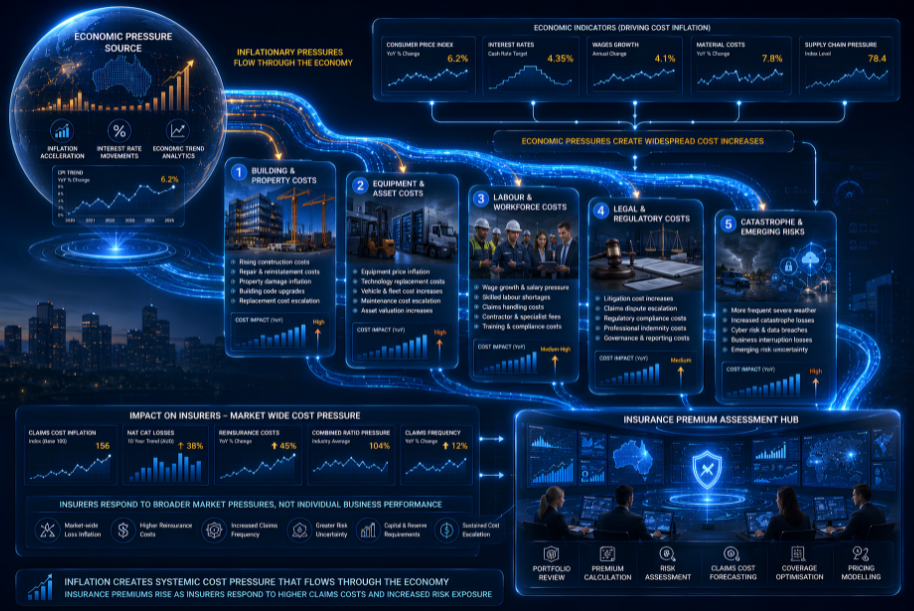

These economic conditions Australia business owners face have a direct impact on insurance requirements.

As business expenses in Australia continue to rise, many organisations attempt to reduce costs wherever possible. However, reducing insurance cover without understanding the potential consequences can create significant exposure.

At the same time, insurers are also responding to increasing claims costs, natural catastrophe losses and evolving risks such as cybercrime.

This combination of higher operating costs and increased insurer caution is contributing to ongoing insurance premium increases Australia businesses are experiencing across multiple sectors.

Businesses should therefore view insurance as part of broader cash flow management and business planning rather than simply another overhead expense.

Are Your Business Assets Properly Insured in Today’s Market?

One of the most common issues we encounter during an insurance policy review is inadequate asset valuation.

Many businesses continue to insure assets based on historic values that may no longer reflect current replacement costs.

This issue is particularly relevant for:

- Buildings

- Machinery

- Plant and equipment

- Inventory

- Fit-outs

- Technology infrastructure

Conducting a sum insured review can help determine whether insured values remain appropriate.

Business owners should consider:

Reviewing Sums Insured and Asset Values

The cost of replacing commercial assets has increased significantly in recent years.

Construction costs, freight charges, labour expenses and material shortages have all contributed to higher replacement values.

A comprehensive insurance valuation review may help identify potential gaps between insured values and actual replacement costs.

Businesses should assess:

- Building replacement values

- Plant and machinery costs

- Stock values

- Equipment replacement expenses

- Technology assets

Accurate business asset valuation insurance practices can help reduce the likelihood of claim disputes and financial shortfalls following a loss.

Failure to conduct regular reviews may result in underinsured business assets, leaving businesses exposed during major claims.

Why More Australian Businesses Are Reviewing Insurance During Changing Interest Rate Conditions

Many organisations are now integrating insurance reviews into broader financial planning activities.

This trend is being driven by:

- Higher financing costs

- Increased operating expenses

- Greater risk awareness

- Rising claims costs

- Evolving regulatory obligations

For many businesses, insurance is no longer viewed as a static annual expense.

Instead, it is becoming a key component of strategic business risk management in Australia.

Across multiple industries, businesses are undertaking:

- Annual policy assessments

- Asset revaluations

- Coverage reviews

- Risk assessments

- Market benchmarking exercises

An effective insurance coverage review can help businesses understand whether their policies remain aligned with their operational realities.

How Inflation and Interest Rates Affect Insurance Premiums?

A common question business owners ask is: why are insurance premiums increasing?

The answer is often linked to broader economic conditions.

The relationship between inflation, business costs, and insurance pricing is significant.

When inflation increases:

- Claim settlement costs rise

- Building repairs become more expensive

- Equipment replacement costs increase

- Labour costs rise

- Legal expenses increase

As insurers absorb higher claims costs, business insurance premiums and commercial insurance premiums may also increase.

This is one of the key drivers behind ongoing rising insurance costs Australia businesses continue to experience.

Businesses should understand that premium increases are not always a result of poor claims history. Often, they reflect wider economic and market factors affecting the entire insurance sector.

The Risk of Underinsurance During Periods of Rising Costs

One of the most significant risks facing Australian businesses today is underinsurance in Australia.

Many businesses fail to adjust insured values as replacement costs increase.

This creates a growing problem of business underinsurance.

When a major loss occurs, businesses may discover their policies no longer provide adequate protection.

Examples include:

- Commercial buildings insured below replacement value

- Equipment insured using outdated valuations

- Stock values not reflecting current inventory costs

- Revenue exposures underestimated for business interruption cover

Underinsurance can result in:

- Reduced claim settlements

- Co-insurance penalties

- Increased out-of-pocket expenses

- Delayed recovery following a loss

Conducting regular replacement cost insurance assessments and asset reviews can help reduce these risks.

Managing Insurance Costs Without Reducing Protection

Although many businesses face pressure to reduce expenditure, cutting insurance cover may not always be the best solution.

Instead, businesses should focus on:

- Risk improvement measures

- Policy optimisation

- Market benchmarking

- Deductible reviews

- Claims management strategies

A professional business insurance audit may uncover opportunities to improve efficiency without compromising protection.

Businesses should also evaluate whether existing policies contain unnecessary overlaps or outdated coverage.

Working with a specialist commercial insurance Australia adviser can often reveal more effective alternatives than simply reducing cover.

Why Business Interruption Cover Matters More Than Ever?

Many businesses focus heavily on physical assets while overlooking revenue protection.

Business interruption insurance Australia can assist businesses facing financial losses following insured events such as:

- Fire

- Storm damage

- Equipment breakdown

- Property damage

- Supply chain disruptions

In today’s economic environment, extended downtime can have a significant impact on profitability and business continuity.

As part of an annual insurance review, businesses should assess whether business interruption periods, gross profit calculations and indemnity limits remain appropriate.

Reviewing Cyber Insurance During Economic Uncertainty

Cyber threats continue to grow regardless of broader economic conditions.

Many businesses are becoming increasingly dependent on technology, remote work arrangements and digital transactions.

As part of an insurance risk assessment business process, organisations should evaluate whether existing cyber insurance Australia policies adequately address:

- Ransomware attacks

- Data breaches

- Business interruption losses

- Cyber extortion

- Regulatory investigations

Economic pressure can sometimes increase cybercrime activity, making cyber protection an important component of modern risk management.

Common Insurance Gaps Australian Businesses Overlook

During an insurance policy review, several recurring issues commonly emerge.

These include:

- Outdated sums insured

- Inadequate liability limits

- Insufficient cyber protection

- Uninsured plant and equipment

- Incorrect business activity descriptions

- Lack of business interruption cover

Businesses should also review key policies such as:

- Public liability insurance Australia

- Commercial property insurance Australia

- Business interruption insurance Australia

- Cyber insurance Australia

Regular reviews can help ensure policies continue to evolve alongside business growth and changing risk profiles.

What To Discuss With Your Insurance Broker Before Renewal

Before your next renewal, it is important to conduct a thorough insurance renewal review.

Business owners should discuss:

- Asset value changes

- Revenue growth

- New contracts

- Additional locations

- Staffing changes

- Technology investments

- Emerging risks

A detailed insurance broker review discussion can help identify areas requiring adjustment before renewal terms are finalised.

Businesses should also consider whether their insurer remains competitive within the broader insurance market in Australia.

Understanding Insurance Market Conditions in Australia

The broader insurance market in Australia continues to experience significant changes.

Factors influencing premiums include:

- Natural catastrophe losses

- Inflation

- Reinsurance costs

- Global economic uncertainty

- Cyber claim frequency

- Supply chain challenges

These trends contribute to:

- Commercial insurance rate increases

- Ongoing insurance market hardening

- Increased underwriting scrutiny

- Higher deductibles

- Stricter policy conditions

Businesses that proactively engage in risk management and policy reviews are often better positioned during renewal negotiations.

Monitoring insurance premium trends in Australia can also help businesses plan future insurance budgets more effectively.

As insurers continue adjusting pricing models, many organisations are also experiencing insurance renewal increases across multiple policy classes.

Review Your Business Insurance Before Your Next Renewal

Periods of changing interest rates create an ideal opportunity to reassess all areas of your business, including insurance.

A professional insurance review in Australia can help ensure your policies remain aligned with current business operations, asset values and risk exposures.

Whether you operate a large enterprise, family business or require small business insurance Australia, SME insurance Australia or specialised coverage for complex industries, a proactive review may help uncover risks before they become costly problems.

At Global Insurance Solutions, we work with business owners insurance Australia needs across a broad range of industries, helping clients navigate evolving market conditions and make informed insurance decisions.

If your business has not undertaken an annual insurance review recently, now may be the time to act.

Speak With Global Insurance Solutions

Our team of business insurance specialists can assist with:

- Comprehensive business insurance review

- Independent insurance policy review

- Coverage benchmarking

- Risk assessments

- Renewal negotiations

- Market comparisons

- Claims advocacy

Whether you require a business insurance quote, support from a business insurance broker Australia, guidance from a commercial insurance broker, or tailored insurance advice for businesses, we can help.

Contact Global Insurance Solutions today for professional insurance renewal assistance and discover why more Australian businesses are choosing to review their business insurance before renewal.

Frequently Asked Questions

Q1. How often should a business insurance policy be reviewed?

Ans 1. Most Australian businesses should review their insurance policies at least annually and whenever significant changes occur, such as purchasing new equipment, expanding operations, increasing revenue, acquiring property, or entering new markets. Regular reviews help ensure cover remains aligned with current business risks.

Q2. Why are business insurance premiums increasing in Australia?

Ans 2. Business insurance premiums may increase due to a range of factors including inflation, higher claims costs, natural disasters, cyber incidents, rising reinsurance costs, and broader insurance market conditions. Premium increases are not always linked to an individual business’s claims history.

Q3. Can rising interest rates affect business insurance costs?

Ans 3. Indirectly, yes. Rising interest rates can increase construction costs, equipment financing expenses, labour costs and replacement values. These factors may contribute to higher sums insured and increased insurance premiums over time.

Q4. What is underinsurance and why is it a concern for Australian businesses?

Ans 4. Underinsurance occurs when the insured value of assets is less than the actual cost to repair, replace or rebuild them. In the event of a claim, businesses may face reduced claim payments, out-of-pocket expenses and potential co-insurance penalties.

Q5. What should be included in a business insurance review?

Ans 5. A business insurance review should assess:

- Asset values and sums insured

- Revenue and business interruption exposures

- Liability limits

- Cyber insurance requirements

- New business activities

- Additional locations

- Changes in staffing or operations

- Emerging risks and contractual obligations

Q6. How can businesses reduce insurance costs without reducing cover?

Ans 6. Businesses may be able to manage insurance costs by improving risk management practices, reviewing deductibles, updating risk information, benchmarking policies against the market and working with an experienced insurance broker to identify suitable alternatives.

Q7. Is business interruption insurance still important in today's economy?

Ans 7. Yes. Business interruption insurance can help businesses recover lost income and ongoing expenses following an insured event. With rising operating costs and economic uncertainty, extended downtime can have a greater financial impact than ever before.

Q8. Should small businesses review their insurance every year?

Ans 8. Yes. Small businesses often experience changes in revenue, staffing, equipment and operations that can affect insurance requirements. An annual review helps ensure cover remains appropriate and up to date.

Q9. What questions should I ask my insurance broker before renewal?

Ans 9. Before renewal, consider discussing:

- Whether asset values remain accurate

- Potential underinsurance concerns

- Changes in business activities

- Emerging cyber and liability risks

- Business interruption calculations

- Market conditions affecting premiums

- Opportunities to improve cover or reduce costs

Q10. Why is now a good time to review business insurance?

Ans 10. Periods of economic change, rising interest rates and increasing operating costs can significantly alter business risks and asset values. Reviewing insurance before renewal can help identify coverage gaps, reduce underinsurance risks and ensure policies continue to meet the needs of the business.

Q11.Can a business insurance broker help negotiate better renewal terms?

Ans 11. A specialist business insurance broker can assist by comparing insurers, negotiating renewal terms, reviewing policy wording, identifying coverage gaps and helping businesses achieve more suitable outcomes at renewal.

Q12. What types of insurance should Australian businesses review regularly?

Ans 12. Businesses should regularly review:

- Public Liability Insurance

- Professional Indemnity Insurance

- Commercial Property Insurance

- Business Interruption Insurance

- Cyber Insurance

- Management Liability Insurance

- Commercial Motor Insurance

- Environmental Liability Insurance

- Workers’ Compensation obligations where applicable

Important notice

This article is of a general nature only and does not take into account your specific objectives, financial situation or needs. It is also not financial advice, nor complete, so please discuss the full details with your insurance broker as to whether these types of insurance are appropriate for you. Deductibles, exclusions and limits apply. You should consider any relevant Target Market Determination and Product Disclosure Statement in deciding whether to buy or renew these types of insurance. Various insurers issue these types of insurance and cover can differ between insurers.

This article provides information rather than financial product or other advice. The content of this article, including any information contained in it, has been prepared without taking into account your objectives, financial situation or needs. You should consider the appropriateness of the information, taking these matters into account, before you act on any information. In particular, you should review the product disclosure statement for any product that the information relates to it before acquiring the product.

Information is current as at the date the article is written as specified within it but is subject to change. Global Insurance Solutions Pty Ltd make no representation as to the accuracy or completeness of the information. Various third parties have contributed to the production of this content. All information is subject to copyright and may not be reproduced without the prior written consent of Global Insurance Solutions Pty Ltd.

Risk Advisor, Insurance Broker & Director

With around 15 years in insurance, Yuvi Singh is a passionate Risk Advisor, Director, and Insurance Broker at Global Insurance Solutions. Backed by a Commerce degree and ANZIIF diploma, Yuvi leads a team servicing SMEs across industries like manufacturing, logistics, fuel, IT, and more. At GIS, clients benefit from tailored, transparent advice, access to 150+ insurers, and end-to-end risk solutions. Recognised as a 2022 Insurance Magazine Rising Star and 2024 Top Insurance Broker by Insurance Business Australia, Yuvi delivers flexible, effective outcomes with integrity and innovation.