For many Australian businesses, the end of the financial year (EOFY) is a time focused on tax planning, accounting, and financial reporting. However, for convenience retailers, service stations, mixed businesses, and fuel retailers, EOFY is also one of the most important times to review business insurance.

Convenience store insurance requirements in Australia continue to evolve as businesses face rising stock costs, cyber threats, inflation, theft risks, and rising operational expenses. Many retailers may unknowingly become underinsured if their policies are not regularly reviewed.

At Global Insurance Solutions, we work with convenience retailers, fuel retailers, and mixed businesses across Australia to help review and arrange tailored insurance solutions designed around their operational risks, business activities, and changing exposures.

Whether you operate an independent convenience store, fuel retail site, mixed retail business, or service station, an EOFY insurance review can help identify potential coverage gaps before they become costly claim issues.

Why EOFY Is the Right Time to Review Retail Insurance?

EOFY naturally aligns with major business reviews including:

- Stocktaking

- Financial reporting

- Revenue assessments

- Equipment upgrades

- Staffing changes

- Lease reviews

- Operational planning

This is an ideal time to review your convenience retailer insurance and ensure your cover still reflects the current size and risk profile of your business.

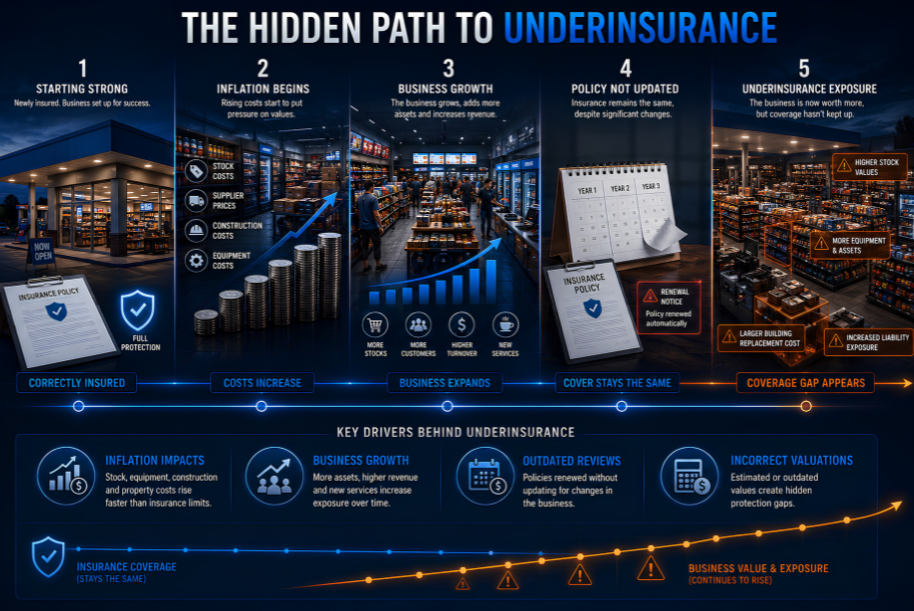

Many retailers only review insurance at renewal time. However, business operations can change significantly throughout the year.

For example:

- Stock values may increase

- Refrigeration equipment may be upgraded

- New services may be added

- Turnover may grow

- Cyber exposure may increase

- Supplier costs may rise

- Property rebuilding costs may escalate

If insurance policies are based on outdated values, businesses may face underinsurance risks Australia-wide.

Recent Federal Budget measures and ongoing insurance market pressures continue to influence rebuilding costs, cyber risks, and insurance affordability for Australian businesses. Learn more in our guide on Federal Budget Information for Aussie Insurance & Business Owners.

According to the Insurance Council of Australia, underinsurance remains a major issue for Australian businesses and property owners due to rising construction and replacement costs.

Source: Insurance Council of Australia

Common Insurance Gaps for Convenience Retailers

Convenience retailers face a wide range of operational and liability risks that are often underestimated.

Some of the most common retail insurance coverage gaps include:

Underinsured Stock Values

Inflation and supplier pricing increases have significantly impacted stock replacement costs across Australia.

Many convenience stores experience seasonal stock fluctuations, meaning stock sums insured may no longer reflect actual exposure levels.

This is especially important for:

- Tobacco stock

- Alcohol products

- Refrigerated products

- Imported goods

- High-value inventory

If stock values are underestimated, claim payouts may be reduced.

Cyber Risks & EFTPOS Fraud

Cyberattacks on retailers continue to increase across Australia.

Convenience stores rely heavily on:

- EFTPOS systems

- Cloud-based POS systems

- Customer payment processing

- Online ordering platforms

- Supplier management systems

The Australian Cyber Security Centre reported over 87,400 cybercrime reports during the 2023–24 financial year, averaging one report every six minutes.

Source: Australian Cyber Security Centre Cyber Threat Report

Retail cyber risks Australia businesses face may include:

- EFTPOS fraud

- Ransomware attacks

- Data breaches

- Business interruption

- Payment system outages

- Customer information theft

Many retailers incorrectly assume standard business insurance automatically covers cyber incidents.

In many cases, separate cyber insurance for retailers may be required.

Business Interruption Gaps

Business interruption insurance retail policies can vary significantly between insurers.

Retailers often overlook:

- Indemnity periods

- Waiting periods

- Excluded events

- Supply chain disruption limitations

- Cyber-related downtime exclusions

A short closure following fire, flood, refrigeration breakdown, or equipment failure can severely impact revenue and cash flow.

Property & Equipment Valuation Issues

Rising rebuilding costs continue to affect commercial property insurance across Australia.

According to CoreLogic, construction costs have increased significantly in recent years due to labour shortages and supply chain pressures.

Source: CoreLogic Construction Cost Insights

Retailers should regularly review:

- Building values

- Refrigeration equipment

- Fit-outs

- Signage

- Glass cover

- Security systems

- Fuel infrastructure

- Plant and machinery

Why Many Retailers Become Underinsured in Australia?

Underinsurance is one of the biggest risks facing convenience retailers.

Several factors contribute to this problem:

Inflation Impacts

Replacement costs for stock, equipment, and commercial property have increased significantly over recent years.

Business Growth

Businesses often expand faster than their insurance arrangements.

Examples include:

- Increased turnover

- New product lines

- Additional staff

- Expanded services

- Store renovations

Outdated Policy Reviews

Some businesses renew policies annually without fully reviewing:

- Sums insured

- Operational changes

- Business activities

- Exposures

- Policy exclusions

Incorrect Valuations

Many retailers estimate values rather than obtaining updated replacement cost assessments.

This can create significant claim shortfalls.

Cyber Risks Facing Convenience Stores

Cyber insurance has become increasingly relevant for convenience retailers and fuel retailers.

Retail businesses are attractive targets because they often process large volumes of financial transactions and customer payment data.

Common cyber exposures include:

- POS system hacking

- Ransomware

- Phishing attacks

- EFTPOS fraud

- Employee error

- Supplier system breaches

- Data theft

The Office of the Australian Information Commissioner (OAIC) continues to report high volumes of notifiable data breaches across Australian organizations.

Source: OAIC Notifiable Data Breaches Report

Cyber insurance for retailers may help cover:

- Incident response costs

- Forensic investigations

- Business interruption losses

- Customer notification expenses

- Legal costs

- Cyber extortion demands

Why Stock & Equipment Values Should Be Reviewed Before EOFY?

EOFY is one of the best times to review stock insurance Australia requirements because businesses are already conducting stocktakes and financial assessments.

Retailers should consider:

Stock Fluctuations

Stock levels may increase due to:

- Seasonal demand

- Supplier pricing

- Bulk purchasing

- Promotional stock

Refrigeration Breakdown Risks

Spoilage insurance and refrigeration breakdown cover may become critical for businesses storing:

- Food

- Dairy

- Frozen products

- Beverages

A refrigeration failure can create significant stock losses within hours.

Machinery Breakdown Exposures

Machinery breakdown insurance may help cover repair or replacement costs for critical operational equipment.

This may include:

- Refrigeration systems

- Air conditioning units

- Fuel pumps

- POS systems

- Compressors

Business Interruption Risks Retailers Often Overlook

Many retailers focus heavily on property damage but underestimate downtime risks.

Business interruption insurance may help cover:

- Loss of income

- Ongoing rent

- Wages

- Utility expenses

- Temporary relocation costs

However, policy wording can vary considerably.

Some retailers may incorrectly assume all interruptions are covered.

In reality, many business interruption claims require physical damage triggers.

For example:

- Fire damage

- Storm damage

- Flood damage

- Machinery breakdown

Certain events may not automatically trigger cover.

This is why reviewing policy wording and exclusions with an insurance broker for convenience stores is important.

What Insurance Should Convenience Retailers Review Before June 30?

Retailers should review several key areas before EOFY:

Property Insurance

Review:

- Building values

- Fit-out costs

- Replacement costs

- Flood exposure

- Storm risks

Public Liability Insurance

Review:

- Customer foot traffic

- Product liability risks

- Contractor exposure

- Limits of liability

Theft Insurance

Review:

- Burglary exposure

- Cigarette stock values

- Cash handling procedures

- Security systems

Cyber Insurance

Review:

- POS systems

- Payment processing exposure

- Data storage

- Employee cyber awareness

Business Interruption Insurance

Review:

- Indemnity periods

- Gross profit calculations

- Revenue exposure

- Supply chain reliance

How Global Insurance Solutions Helps Convenience Retailers Australia-Wide?

At Global Insurance Solutions, we work with convenience retailers, mixed businesses, and fuel retail operators across Australia.

We understand the operational risks convenience retailers commonly face, including:

- Theft and burglary

- Cyber risks

- Stock losses

- Refrigeration breakdown

- Storm and flood damage

- Business interruption

- Liability exposures

Our team helps businesses review:

- Existing insurance structures

- Policy wording

- Sums insured

- Coverage gaps

- Operational risks

- Claims preparedness

As an insurance broker agency serving Australia-wide, we help convenience retailers access tailored insurance solutions designed around their business operations and industry exposures.

Conclusion

An EOFY insurance review is not just an administrative exercise.

For convenience retailers, service stations, and mixed businesses, it can help identify underinsurance risks, outdated policy structures, cyber exposures, and operational gaps before claims occur.

With rising replacement costs, increasing cyber threats, and evolving insurer requirements, reviewing insurance annually has become increasingly important for Australian retailers.

At Global Insurance Solutions, we work with businesses across Australia to help review retail insurance programs and support businesses operating in high-risk retail environments.

Frequently Asked Questions

Q1. Why should convenience retailers review insurance before EOFY?

A1. EOFY is a practical time to review stock levels, turnover, equipment values, staffing changes, and operational risks to ensure insurance cover still aligns with the business.

Q2. What insurance does a convenience store need in Australia?

A2. Convenience stores commonly require public liability insurance, commercial property insurance, theft cover, cyber insurance, business interruption insurance, glass cover, and machinery breakdown insurance.

Q3. Why are convenience retailers at risk of underinsurance?

A3. Rising replacement costs, inflation, stock increases, and growing business operations can cause businesses to become underinsured if policies are not regularly reviewed.

Q4. Does convenience store insurance cover theft?

A4. Many policies may include theft and burglary cover, although policy limits, security conditions, and exclusions may apply.

Q5. What is business interruption insurance for retailers?

A5. Business interruption insurance may help cover loss of income and ongoing expenses if the business cannot operate following an insured event.

Q6. Does retail insurance cover cyber attacks?

A6. Standard retail insurance may not automatically cover cyber incidents. Separate cyber insurance may help cover ransomware attacks, data breaches, EFTPOS fraud, and cyber-related business interruption.

Q7. What should retailers review during an EOFY insurance review?

A7. Retailers should review stock sums insured, turnover, staffing, business activities, cyber risks, property values, equipment, and policy exclusions.

Q8. How often should convenience retailers review insurance?

A8. Insurance should generally be reviewed annually and whenever significant business changes occur.

Q9. Why are retail insurance premiums increasing in Australia?

A9. Premium increases may result from inflation, severe weather events, cyber incidents, theft risks, rising rebuilding costs, and changing insurer risk assessments.

Q10. Can Global Insurance Solutions help convenience retailers across Australia?

A10. Yes. Global Insurance Solutions works with convenience retailers, mixed businesses, and fuel retail operators across Australia to help review and arrange tailored insurance solutions.

Important notice

This article is of a general nature only and does not take into account your specific objectives, financial situation or needs. It is also not financial advice, nor complete, so please discuss the full details with your insurance broker as to whether these types of insurance are appropriate for you. Deductibles, exclusions and limits apply. You should consider any relevant Target Market Determination and Product Disclosure Statement in deciding whether to buy or renew these types of insurance. Various insurers issue these types of insurance and cover can differ between insurers.

This article provides information rather than financial product or other advice. The content of this article, including any information contained in it, has been prepared without taking into account your objectives, financial situation or needs. You should consider the appropriateness of the information, taking these matters into account, before you act on any information. In particular, you should review the product disclosure statement for any product that the information relates to it before acquiring the product.

Information is current as at the date the article is written as specified within it but is subject to change. Global Insurance Solutions Pty Ltd make no representation as to the accuracy or completeness of the information. Various third parties have contributed to the production of this content. All information is subject to copyright and may not be reproduced without the prior written consent of Global Insurance Solutions Pty Ltd.

Risk Advisor, Insurance Broker & Director

With around 15 years in insurance, Yuvi Singh is a passionate Risk Advisor, Director, and Insurance Broker at Global Insurance Solutions. Backed by a Commerce degree and ANZIIF diploma, Yuvi leads a team servicing SMEs across industries like manufacturing, logistics, fuel, IT, and more. At GIS, clients benefit from tailored, transparent advice, access to 150+ insurers, and end-to-end risk solutions. Recognised as a 2022 Insurance Magazine Rising Star and 2024 Top Insurance Broker by Insurance Business Australia, Yuvi delivers flexible, effective outcomes with integrity and innovation.