Imagine this.

It’s Monday morning.

Your fuel delivery doesn’t arrive.

Customers line up. Pumps run dry. Staff scrambles to manage frustrated drivers. By midday, your servo is effectively shut.

By Friday, the question isn’t just “Where is the fuel?”

It’s “How much revenue have we lost… and will insurance cover it?”

This is the reality many Australian service stations could face amid global supply chain disruption, geopolitical conflict, and fuel shortages.

And here’s the uncomfortable truth:

Most business interruption insurance claims Australia businesses expect to be covered… are not.

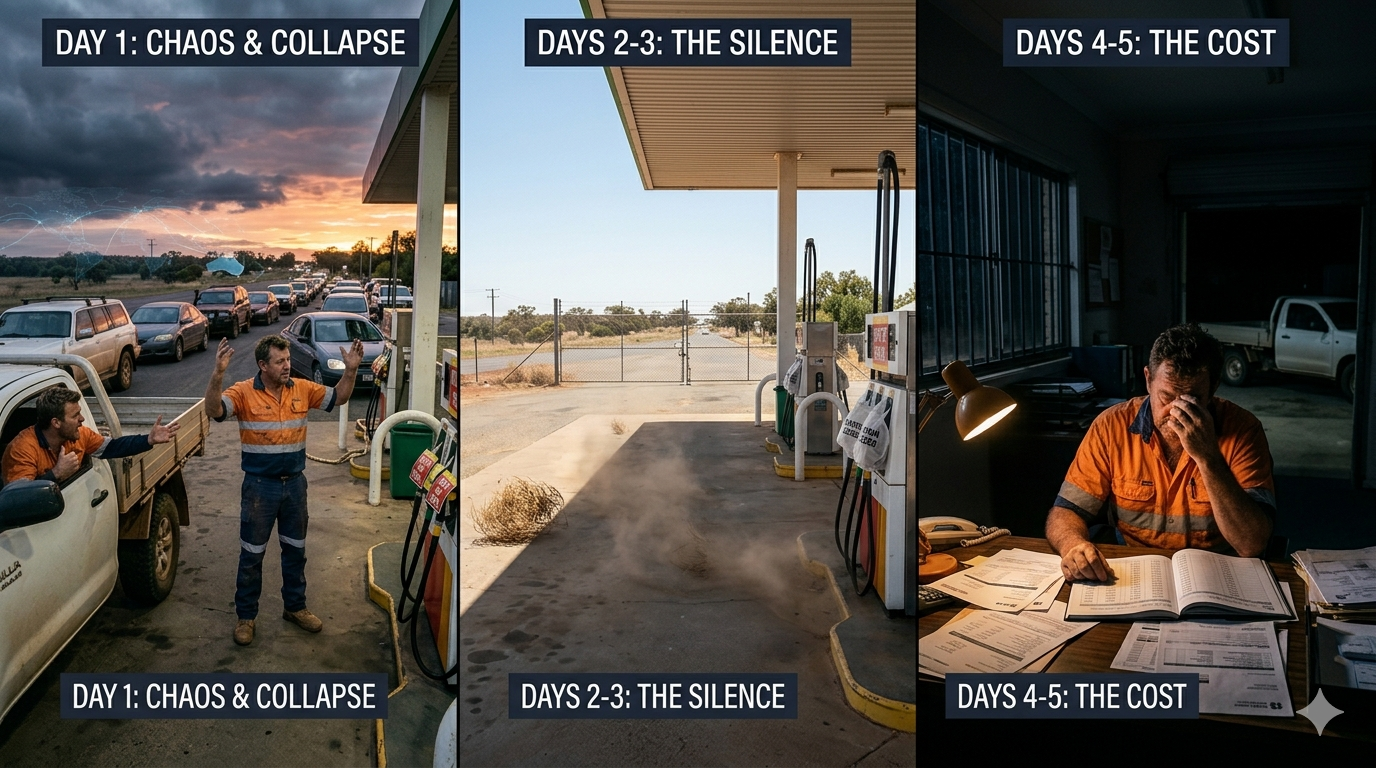

Day-by-Day Breakdown: What Happens When a Servo Stops Trading

Day 1: Panic + Customer Chaos

Fuel tanks run low. Social media spreads the word. Queues build.

You start rationing fuel or shut pumps completely.

Immediate impact:

- Lost sales

- Customer dissatisfaction

- Brand damage

Day 2–3: Revenue Collapse

No fuel = no foot traffic.

Your shop sales drop. Coffee sales disappear.

Your business model collapses overnight.

This is where owners start asking: “Does business interruption cover loss of income in Australia?”

Day 4–5: Staff + Cash Flow Pressure

You still have:

- Wages to pay

- Rent or loan repayments

- Supplier obligations

But no revenue.

Cash flow stress begins. Decisions become reactive.

The Insurance Reality Check

Here’s where things get critical.

Many servo owners assume: “If I lose revenue, my insurance will cover it.”

That assumption is often wrong.

Revenue Decline vs Insured Interruption

Key Concept Most Businesses Misunderstand

Business interruption insurance does NOT cover all revenue loss.

It typically only responds when there is:

✔ A trigger event

✔ Causing physical damage

✔ Leading to interruption of business

So What Doesn’t Count?

- A drop in fuel demand due to the economic slowdown

- Supply chain delays without physical damage

- Shipping disruptions due to geopolitical conflict

- Customer behaviour changes

These fall under uninsured business risks, not insured events.

What Triggers a Business Interruption Claim?

This is one of the most searched questions:

“What triggers a business interruption claim?”

To claim successfully, you generally need:

1. Physical Damage

Example:

- Fire damaged fuel pumps

- Storm destroying the canopy or tanks

2. Insured Event

The damage must be caused by an insured peril, such as:

- Fire

- Storm

- Explosion

3. Direct Link to Interruption

The damage must directly prevent trading.

Without these, business interruption insurance supply chain disruption scenarios are often NOT covered.

Does Business Interruption Cover Supply Chain Disruption?

Short answer: Usually NO

Unless your policy includes specific extensions such as:

Contingent Business Interruption

Covers losses caused by:

- Supplier disruption

- Key customer shutdown

Denial of Access

Covers situations where:

- Authorities prevent access to your premises

Prevention of Access

Triggered when:

- External events stop operations

However…

Even these extensions often require physical damage to the supplier or nearby property.

Fuel Shortage Scenario: The Coverage Gap

Scenario: Shipping Delays Due to Global Conflict

A geopolitical conflict disrupts fuel imports. Your supplier cannot deliver for 5 days.

Impact:

- No fuel supply

- Business shutdown

- Revenue loss

Will Insurance Cover It?

In most cases: NO, Why?

- No physical damage

- No insured trigger event

- Pure supply chain disruption

Relevant Search Query Answered

“Does insurance cover supply chain delays?”

Not unless specifically endorsed.

Real Business Interruption Claims Examples Australia

Let’s break this down with real-world style comparisons.

Covered Scenario

A fire damages underground fuel tanks.

✔ Physical damage

✔ Insured event

✔ Business shuts down

Claim likely paid

Not Covered Scenario

Fuel supply stops due to shipping delays.

✘ No damage

✘ No insured event

Claim likely denied

Why Business Interruption Claims Get Rejected

This is where frustration builds.

Common reasons:

1. No Trigger Event

No physical damage = no claim

2. Policy Exclusions

Many policies clearly exclude:

- Supply chain disruption

- Economic downturn

3. Misunderstanding Coverage

Businesses assume: “Loss of revenue = covered”

But policies are structured differently.

Business Interruption Insurance Exclusions Australia

Typical exclusions include:

- Market conditions or reduced demand

- Supplier failure without damage

- Pandemic-related shutdowns (in many policies)

- Utility failures (unless extended)

This is why business interruption insurance exclusions in Australia are one of the most searched topics.

Can You Claim Business Interruption Without Property Damage?

In most standard policies: NO

However, some advanced policies may include:

- Non-damage business interruption

- Supply chain extensions

- Cyber-triggered interruption

What If Your Servo Can’t Trade Tomorrow?

Let’s explore real risks beyond fuel shortage.

Scenario 1: Cyber Attack

A cyber attack hits your servo during peak trading hours. Malware infiltrates your network, shutting down fuel pumps, EFTPOS terminals, and back-office systems. Customers are left stranded at the bowser, queues build up, and staff are forced to turn people away.

Unlike traditional property damage events, there is no physical loss or damage to trigger a standard business interruption claim. The loss is purely digital, but the financial impact is very real.

Your business may face:

- Immediate loss of fuel and shop revenue

- System restoration and IT forensic costs

- Ransom demands or extortion payments

- Reputational damage and customer distrust

- Ongoing downtime is impacting cash flow

Covered under: Cyber Insurance

A properly structured cyber policy can respond to:

- Business interruption from system outages

- Incident response and recovery costs

- Cyber extortion and ransomware events

- Data breach notification and regulatory obligations

- Not covered under standard Business Interruption

Most traditional business interruption policies require physical damage to insured property to trigger a claim. A cyber event, even if it shuts down your entire operation, often falls outside this definition.

Key takeaway: If your servo relies on digital systems to trade (which most do), a cyber attack can stop revenue instantly. Without cyber insurance, you could be absorbing the full financial impact of a shutdown that lasts days or even weeks.

Scenario 2 – Electricity Failure

A sudden power outage hits your area. Fuel pumps stop working, POS systems go offline, refrigeration units shut down, and your entire operation comes to a standstill. Even if fuel is available, you cannot dispense it or process payments.

What seems like a simple outage can quickly escalate into a serious financial issue.

Your business may face:

- Immediate loss of fuel and shop sales

- Spoilage of refrigerated stock

- Customer walkaways and reputational impact

- Ongoing fixed costs with no incoming revenue

Coverage depends on policy extensions

Whether you are covered comes down to how your policy is structured.

Some policies may include:

- Business Interruption with utility services extension: Covers loss of income due to failure of the electricity, gas, or water supply

- Prevention of access or closure by a public authority: May respond if the outage is linked to a broader incident or safety issue

- Deterioration of stock cover: Protects against the spoilage of perishable goods due to a power failure

However, many standard policies:

- Do not automatically include utility failure cover

- May only respond if the outage is caused by physical damage at the supply source

- Can exclude short-term outages or impose waiting periods

Key takeaway: Not all power outages are treated equally under insurance. Without the right extensions, a full shutdown of your servo may result in zero claim payout. The difference often comes down to a single clause in your policy wording.

Scenario 3 – Fuel Contamination

Fuel contamination can occur without warning. Water ingress, sediment build-up, or supplier issues can render your entire fuel stock unusable overnight. Vehicles may stall after refuelling, leading to customer complaints, potential liability claims, and immediate shutdown of affected pumps.

In many cases, servos are forced to stop selling fuel altogether until tanks are drained, cleaned, and refilled.

Your business may face:

- Loss of saleable fuel stock

- Cost of tank cleaning and disposal

- Customer claims for vehicle damage

- Business interruption during shutdown

- Reputational damage impacting repeat customers

May be covered under: Property Damage / Stock Contamination

Coverage depends heavily on the cause and policy wording.

Some policies may respond under:

- Property damage: If contamination is caused by an insured event, such as tank damage, storm, or accidental ingress

- Stock contamination or deterioration cover: Designed to cover the loss of stock that becomes unsafe or unusable

- Environmental or pollution liability (in some cases): If contamination leads to environmental damage or third-party impact

However, many policies:

- Exclude gradual contamination or maintenance-related issues

- May not cover supplier-related quality issues

- Require a clearly defined insured event to trigger a claim

Key takeaway: Fuel contamination is one of the most overlooked risks in servo operations. Without the right cover, you may be left paying for lost fuel, clean-up costs, and customer claims out of pocket. The trigger for cover is not the loss itself, but what caused it.

This highlights why the servo insurance business interruption cover must be structured correctly.

The Cost of Getting It Wrong

According to the Insurance Council of Australia, business interruption losses are one of the largest components of commercial claims.

🔗 https://insurancecouncil.com.au

Additionally, Allianz Global Corporate & Speciality Risk Barometer consistently ranks business interruption as the #1 business risk globally.

🔗 https://www.agcs.allianz.com/news-and-insights/reports/allianz-risk-barometer.html

Yet most SMEs remain underinsured or incorrectly structured.

Common Business Interruption Insurance Mistakes

- Buying cover based on price

- Not understanding trigger events

- Ignoring supply chain risk

- No cyber coverage

- No broker guidance

The Role of a Specialist Broker

At Global Insurance Solutions, we don’t just arrange policies.

We:

- Identify hidden coverage gaps

- Structure policies for real-world risks

- Negotiate tailored extensions

- Support claims when it matters most

Especially for:

- Petrol stations

- Fuel distributors

- High-risk businesses

How to Protect Your Servo Business Properly

To reduce risk exposure, consider:

1. Review Your Business Interruption Policy

Most servo owners assume business interruption insurance will respond whenever revenue drops. The reality is very different. BI cover is one of the most misunderstood areas of insurance, and this is where claims are often denied.

Understand what triggers a claim

Business interruption insurance is not designed to cover every loss of income. It is typically triggered by:

- Physical damage to insured property (for example, fire, storm, or impact)

- Damage that directly prevents your business from trading

- Events specifically listed in your policy wording

In some cases, the cover can be extended to include:

- Utility failures (electricity, water, gas)

- Prevention of access

- Infectious disease or closure orders

But these only apply if they are explicitly included.

Understand what is excluded

This is where most gaps occur. Common exclusions include:

- Revenue decline due to economic conditions or reduced demand

- Supply chain disruptions without physical damage

- Cyber events (unless separately insured)

- Equipment breakdown not listed as an insured event

- Gradual issues such as wear, tear, or maintenance failures

Even where cover exists, policies may include:

- Waiting periods before cover starts

- Sub-limits that reduce the payout

- Strict definitions of what constitutes “damage”

Key takeaway: Business interruption insurance does not cover “loss of income” in general. It covers loss of income resulting from specific insured events. If you do not understand those triggers and exclusions, you may only discover the gap when a claim is declined.

2. Add Supply Chain Extensions

Many servos rely heavily on consistent fuel deliveries and supplier networks. When that supply chain is disrupted, even without damage at your premises, your ability to trade can stop instantly.

Where available?

Some insurers offer supply chain or contingent business interruption extensions, designed to cover losses arising from disruptions outside your direct control.

These extensions may respond to:

- Damage at a supplier’s premises (e.g. refinery, terminal, distributor)

- Transport disruptions impacting fuel delivery

- Port closures, shipping delays, or logistics breakdowns

- A key supplier failure is preventing the stock supply

However, cover is not automatic and is often:

- Limited to named suppliers only

- Triggered only when there is physical damage at the supplier’s location

- Subject to tight sub-limits and conditions

- Excluding broader geopolitical or economic disruptions

Without this extension, a scenario where your fuel simply does not arrive, even for several days, may not trigger any claim under standard BI cover.

Key takeaway: If your revenue depends on third-party supply, your insurance should reflect that dependency. Supply chain extensions can bridge a critical gap, but only if they are correctly structured and aligned with how your business actually operates.

3. Consider Cyber Insurance

Modern servos are no longer just fuel retailers. They are digitally driven operations relying on POS systems, payment gateways, fuel pump controllers, and back-office software. When these systems fail due to a cyber event, your ability to trade can stop instantly.

For operational shutdown risks

A cyber incident can shut down your operations without any physical damage, which means standard business interruption insurance is unlikely to respond.

Common cyber-related shutdown scenarios include:

- Ransomware attacks are locking fuel pump systems

- POS and EFTPOS outages are preventing transactions

- Network breaches are forcing systems offline

- Third-party provider failures (e.g. payment processors or cloud systems)

- Cyber insurance is designed to respond to these risks and may cover:

- Business interruption losses from system downtime

- Incident response costs, including IT forensics and recovery

- Cyber extortion and ransomware payments

- Data breach notification and regulatory costs

- Third-party liability if customer data is compromised

- Without cyber cover, even a short outage can result in:

- Immediate revenue loss

- Ongoing fixed expenses with no income

- Significant recovery costs

Key takeaway: If your servo relies on technology to operate, a cyber event is not just an IT issue; it is a business-interruption risk. Cyber insurance fills a critical gap that traditional policies often leave exposed.

4. Work With a Specialist Broker

Not all insurance policies are created equal, especially when it comes to complex risks like business interruption, cyber events, and supply chain disruption. Two policies may look similar on price, but the wording, triggers, and exclusions can be vastly different.

A specialist broker understands how servos actually operate and where the real risks sit. They help you:

- Identify hidden gaps in standard policies

- Structure covers correctly across BI, cyber, property, and liability

- Compare insurers beyond price, focusing on coverage quality

- Negotiate tailored extensions, such as utility failure or supply chain cover

- Align sums insured and indemnity periods with real cash flow exposure

Most importantly, a broker supports you when a claim arises, ensuring the policy responds as intended and advocating on your behalf.

Without expert guidance, many businesses:

- Assume they are covered for events that are actually excluded

- Underinsure key areas like business interruption

- Miss critical extensions that could determine whether a claim is paid

At Global Insurance Solutions, we work with servo operators across Australia to structure policies that reflect real operational risks, not just standard insurer templates. With access to 150+ insurers and industry-recognised expertise, we focus on delivering tailored cover, identifying hidden exclusions, and ensuring your policy performs when it matters most.

We do not just arrange an insurance policy. We advocate for you at every stage, from initial steps through to complex claims, so you are not left dealing with insurers alone.

Key takeaway: Insurance is not just about having a policy. It is about having the right structure. Working with a specialist broker ensures your cover reflects real-world risks, not just generic policy wording.

To learn more about Servo Insurance & how it works, tap to know more.

Final Conclusion

Here’s the reality:

- Business interruption insurance doesn’t fail when claims are denied.

- It fails when it’s structured incorrectly from the start.

And in today’s world of fuel shortages, geopolitical risk, and supply chain disruption, that gap is wider than ever.

Speak to our Servo Insurance Specialist Now

We’ve curated a range of blogs focused on servos.

You can explore them here to better understand the challenges and how the right insurance can help address them.

FAQs

Q1. Does business interruption insurance cover loss of customers?

Ans 1. No. Standard policies do not cover loss of customers or reduced demand unless linked to an insured event causing damage.

Q2. What triggers a business interruption claim?

A claim is triggered by physical damage caused by an insured event that directly interrupts business operations.

Q3. Does business interruption cover supply chain disruption?

Ans 3. Generally, no, unless your policy includes contingent business interruption or specific extensions.

Q4. Can you claim business interruption without physical damage?

Ans 4. In most cases, no. Only specialised policies or extensions may allow this.

Q5. What is not covered under business interruption insurance?

Ans 5. Common exclusions include economic downturns, supplier delays, pandemics, and market conditions.

Q6. Does insurance cover the cyber shutdown of a business?

Ans 6. Not under standard BI policies. This requires a dedicated cyber insurance policy.

Q7. How long does business interruption insurance pay

Ans 7. It depends on your indemnity period, typically ranging from 6 to 24 months.

Important notice

This article is of a general nature only and does not take into account your specific objectives, financial situation or needs. It is also not financial advice, nor complete, so please discuss the full details with your insurance broker as to whether these types of insurance are appropriate for you. Deductibles, exclusions and limits apply. You should consider any relevant Target Market Determination and Product Disclosure Statement in deciding whether to buy or renew these types of insurance. Various insurers issue these types of insurance and cover can differ between insurers.

This article provides information rather than financial product or other advice. The content of this article, including any information contained in it, has been prepared without taking into account your objectives, financial situation or needs. You should consider the appropriateness of the information, taking these matters into account, before you act on any information. In particular, you should review the product disclosure statement for any product that the information relates to it before acquiring the product.

Information is current as at the date the article is written as specified within it but is subject to change. Global Insurance Solutions Pty Ltd make no representation as to the accuracy or completeness of the information. Various third parties have contributed to the production of this content. All information is subject to copyright and may not be reproduced without the prior written consent of Global Insurance Solutions Pty Ltd.

Risk Advisor, Insurance Broker & Director

With around 15 years in insurance, Yuvi Singh is a passionate Risk Advisor, Director, and Insurance Broker at Global Insurance Solutions. Backed by a Commerce degree and ANZIIF diploma, Yuvi leads a team servicing SMEs across industries like manufacturing, logistics, fuel, IT, and more. At GIS, clients benefit from tailored, transparent advice, access to 150+ insurers, and end-to-end risk solutions. Recognised as a 2022 Insurance Magazine Rising Star and 2024 Top Insurance Broker by Insurance Business Australia, Yuvi delivers flexible, effective outcomes with integrity and innovation.