Running an independent fuel retail business in Australia comes with far more risk than many operators realise. From fuel contamination and underground tank exposure to cyber attacks on POS systems and public liability claims, independent fuel retailers face operational, environmental, and financial risks every day.

Whether you operate a single service station, multiple fuel sites, or a regional independent servo, having the right independent fuel retailer insurance, fuel retailer insurance Australia, and service station insurance strategy is critical to protecting your business.

At Global Insurance Solutions, we work with independent fuel retailers across Australia to structure tailored insurance solutions that align with the real risks facing the fuel industry. Many standard business insurance policies fail to properly address fuel-related exposures, environmental liabilities, cyber risks, and operational downtime.

In this guide, we explain what insurance independent fuel retailers actually need, the common gaps businesses overlook, and how specialist fuel industry insurance can help protect long-term business continuity.

Why Independent Fuel Retailers Face Unique Insurance Risks?

Fuel retailers operate in one of Australia’s highest-risk retail environments.

Unlike standard retail businesses, petrol stations and service stations manage hazardous goods, flammable materials, underground infrastructure, fuel transport exposure, and high daily customer volumes.

Some of the most common fuel station business risks include:

- Fuel leaks and environmental contamination

- Underground tank failures

- Public slip-and-fall incidents

- Fire and explosion risks

- Fuel theft and drive-offs

- Equipment and pump breakdowns

- Cyber attacks targeting payment systems

- Supply chain disruption affecting fuel availability

- Contractor liability risks

- Business interruption from storms or power outages

According to the Australian Institute of Petroleum, Australia operates more than 6,800 retail fuel sites nationally, many of which are independently owned or operated.

Source: https://aip.com.au/

Additionally, cyber attacks continue to rise across Australian businesses. The Australian Cyber Security Centre (ACSC) reported over 94,000 cybercrime reports in a single financial year, equating to one report every six minutes.

Source: https://www.cyber.gov.au/

For fuel retailers relying heavily on payment systems, POS infrastructure, and digital operations, the exposure is significant.

This is why standard business cover is often insufficient for fuel businesses.

Essential Insurance Policies for Fuel Retailers

Public Liability Insurance for Fuel Retailers

One of the most critical forms of insurance for independent fuel retailers is public liability insurance.

Fuel stations experience constant foot traffic, vehicle movement, and customer interaction. This creates substantial liability exposure.

A customer could:

- Slip on a fuel spill

- Trip over damaged forecourt surfaces

- Suffer injury during refuelling

- Experience vehicle damage from faulty equipment

Without proper public liability insurance for fuel retailers, these incidents can lead to expensive legal costs and compensation claims.

Many independent operators underestimate how quickly liability claims can escalate, particularly where serious injury occurs.

Your policy should be tailored specifically for:

- Petrol station operations

- Forecourt activities

- Hazardous goods exposure

- Car wash facilities

- Convenience store operations

- Third-party contractor activities

2. Commercial Property Insurance for Service Stations

Fuel retailers often have millions invested in buildings, pumps, canopies, refrigeration systems, stock, signage, and underground infrastructure.

Comprehensive property insurance for service stations can help protect against:

- Fire damage

- Storm and flood damage

- Theft and vandalism

- Machinery damage

- Electrical failures

- Impact damage

Many operators also require ISR insurance.

ISR stands for Industrial Special Risks insurance and is commonly used for larger or multi-site fuel businesses.

A properly structured ISR insurance for petrol stations policy may provide broader protection compared to standard commercial property insurance.

You can learn more about tailored commercial property solutions here: Commercial Property Insurance

3. Environmental Liability Insurance and Fuel Contamination Risks

Environmental exposure is one of the biggest risks facing fuel retailers.

Even a small fuel leak can result in:

- Soil contamination

- Groundwater pollution

- Environmental regulator investigations

- Expensive clean-up costs

- Third-party claims

- Business shutdowns

This is where environmental liability insurance for fuel stations becomes essential.

Many fuel retailers incorrectly assume public liability insurance automatically covers pollution incidents. In reality, gradual pollution and contamination are often excluded.

Specialised cover may include:

- Fuel contamination insurance

- Pollution liability insurance

- Underground tank insurance

- Clean-up and remediation costs

- Environmental legal defence costs

- Emergency response expenses

The Australian Government highlights that contaminated site remediation can involve substantial environmental and financial consequences.

Source: https://www.dcceew.gov.au/

For independent fuel retailers, environmental claims can threaten the survival of the business if uninsured.

Learn more about Fuel Contamination Insurance from here.

4. Cyber Insurance for Petrol Stations

Modern service stations are increasingly reliant on technology.

Today’s independent fuel retailers use:

- POS systems

- Digital payment gateways

- Fuel monitoring systems

- Customer loyalty programs

- Cloud-based reporting systems

- Supplier management platforms

This creates major fuel retailer cyber risk exposure.

Cyber criminals increasingly target retail businesses using ransomware, phishing attacks, and payment system breaches.

According to IBM’s Cost of a Data Breach Report 2023, the global average cost of a data breach reached USD $4.45 million.

Source: https://www.ibm.com/reports/data-breach

Specialist cyber insurance for petrol stations may help cover:

- Data breaches

- Ransomware attacks

- Business interruption from cyber events

- Regulatory investigations

- Customer notification costs

- Digital forensic investigations

- Cyber extortion demands

Many fuel retailers wrongly assume cyber attacks only affect large corporations.

In reality, independent businesses are often targeted because they may have weaker security controls.

Learn more about cyber protection here: Cyber Insurance

Business Interruption Insurance for Service Stations

A fuel retailer does not need to suffer a total fire loss to experience severe financial disruption.

Operational downtime can occur due to:

- Storm damage

- Pump failures

- Refrigeration breakdown

- Fuel contamination

- Cyber incidents

- Power outages

- Supplier disruptions

This is why business interruption insurance for fuel retailers is critical.

Business interruption insurance may help cover:

- Loss of gross profit

- Ongoing operating expenses

- Employee wages

- Temporary relocation costs

- Increased cost of working

However, many fuel retailers discover too late that their policy wording contains major limitations.

For example:

- Supply chain disruptions may not be automatically covered

- Cyber-related downtime may be excluded

- Waiting periods can apply

- Underinsurance can reduce claim payouts

This is particularly important given ongoing global fuel supply chain volatility and operational dependency.

Properly structuring indemnity periods and revenue calculations is essential for fuel retailers.

Workers' Compensation Insurance in the Fuel Industry

Fuel retail businesses often employ:

- Console operators

- Forecourt attendants

- Drivers

- Store staff

- Cleaners

- Maintenance personnel

The fuel industry presents increased workplace injury risks, including:

- Slips and falls

- Manual handling injuries

- Chemical exposure

- Vehicle-related accidents

- Fatigue-related incidents

Workers’ compensation insurance in the fuel industry is legally required across Australia and plays a key role in protecting both employees and business continuity.

Strong workplace safety and risk management practices can also positively influence insurance outcomes and claims history.

Management Liability Insurance for Fuel Retailers

Independent fuel retailers also face management and governance risks.

Owners and directors can face claims involving:

- Employment disputes

- Unfair dismissal

- Workplace harassment allegations

- Regulatory investigations

- Taxation disputes

- WHS breaches

This is why many operators choose management liability insurance for fuel retailers.

Management liability insurance may help protect:

- Directors and officers

- The business entity itself

- Senior management personnel

Learn more here: Management Liability Insurance

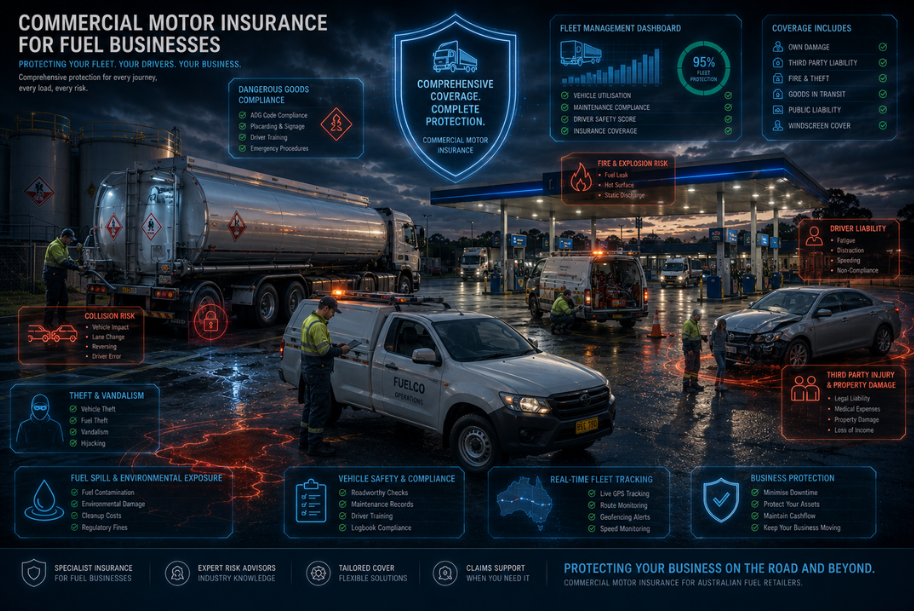

Commercial Motor Insurance for Fuel Businesses

Many fuel retailers operate:

- Fuel delivery vehicles

- Maintenance vehicles

- Company utes

- Fleet vehicles

Comprehensive commercial motor insurance fuel business cover may help protect against:

- Vehicle accidents

- Property damage

- Third-party injury claims

- Theft

- Fire

- Driver liability exposure

Fuel transport exposure can create additional dangerous goods liability considerations that standard vehicle policies may not properly address.

Common Insurance Gaps Fuel Retailers Overlook

Many fuel retailers believe they are insured until a claim occurs.

Some of the most common gaps include:

Underinsurance

Rising construction and replacement costs mean many service stations are significantly underinsured.

According to the Insurance Council of Australia, underinsurance remains a major issue across Australian businesses and property owners.

Source: https://insurancecouncil.com.au/

Environmental Exclusions

Many standard policies exclude:

- Gradual pollution

- Long-term contamination

- Groundwater damage

- Tank seepage

Cyber Exclusions

Traditional policies often exclude:

- Cyber attacks

- Payment fraud

- Ransomware

- Data restoration costs

Without dedicated cyber insurance, businesses may remain exposed.

Read the full information about cyber exclusions here.

Inadequate Business Interruption Cover

Many businesses fail to:

- Accurately calculate gross profit

- Structure adequate indemnity periods

- Include supplier disruption exposure

- Cover operational downtime properly

Poor Risk Management Practices

Insurers may reduce or decline claims where businesses fail to maintain:

- Tank inspections

- Environmental controls

- Cyber security measures

- Equipment maintenance

- Safety procedures

Why Specialist Fuel Industry Insurance Matters?

Fuel retail businesses are not standard retail operations.

They involve:

- Hazardous goods exposure

- Environmental liability

- Complex compliance obligations

- Cyber risk

- High-value infrastructure

- Operational dependency

This is why working with a specialist fuel retailer insurance broker matters.

A broker experienced in specialist fuel industry insurance can help:

- Identify hidden risks

- Structure-tailored cover

- Compare insurer wording

- Negotiate broader protection

- Assist with claims advocacy

- Review operational exposures regularly

How Global Insurance Solutions Supports Independent Fuel Retailers?

At Global Insurance Solutions, we work with independent fuel retailers, service stations, and petrol station operators across Australia.

Our team helps businesses structure:

- Tailored insurance for petrol stations

- Environmental liability protection

- Cyber insurance solutions

- Commercial property insurance

- Business interruption insurance

- Management liability protection

- Workers compensation strategies

- Fuel retail risk management insurance

We understand the operational realities facing fuel retailers and help businesses avoid generic insurance solutions that may leave critical gaps uncovered.

Explore our specialist servo insurance solutions here: Servo Insurance Australia

Whether you operate in Melbourne, Sydney, Brisbane, Perth, Adelaide, or regional Australia, our team provides Australia-wide fuel insurance solutions designed around your business risks.

Final Thoughts

Independent fuel retailers face some of the most complex business risks in Australia.

From environmental exposure and cyber attacks to fuel contamination and operational downtime, the consequences of inadequate insurance can be financially devastating.

The right insurance strategy is not simply about price. It is about ensuring your business is properly protected when a major incident occurs.

A tailored insurance review can help identify:

- Coverage gaps

- Underinsurance exposure

- Environmental liabilities

- Cyber vulnerabilities

- Business interruption weaknesses

For independent fuel retailers, specialist insurance advice matters.

What insurance do independent fuel retailers need in Australia?

Independent fuel retailers typically require public liability insurance, commercial property insurance, environmental liability insurance, cyber insurance, business interruption insurance, workers’ compensation, and management liability insurance.

FAQs

Q1. Is environmental liability insurance important for petrol stations?

Ans 1. Yes. Fuel leaks, contamination, and pollution incidents can result in significant cleanup costs, legal liabilities, and regulatory action for fuel retailers in Australia.

Q2. Why do fuel retailers need cyber insurance?

Ans 2. Modern service stations rely heavily on POS systems, payment gateways, and customer data. Cyber insurance helps protect against ransomware, payment fraud, and data breaches.

Q3. Does business interruption insurance cover fuel supply disruptions?

Ans 3. Not always. Coverage depends on policy wording and whether contingent business interruption or supply chain disruptions are included.

Q4. What risks are commonly excluded from fuel retailer insurance policies?

Ans 4. Common exclusions may include underinsurance, gradual pollution, cyber incidents without endorsements, poor maintenance, and uninsured supplier disruptions.

Q5. Can independent fuel retailers customise their insurance policies?

Ans 5. Yes. A specialist insurance broker can tailor cover based on the size of the operation, fuel storage, retail services, and business risks.

Q6. What is the difference between servo insurance and standard business insurance?

Ans 6. Servo insurance is specifically designed for fuel retailers and can include specialised cover for underground tanks, environmental risks, fuel contamination, and hazardous goods exposures.

Q7. How can Global Insurance Solutions help fuel retailers?

Ans 7. Global Insurance Solutions helps independent fuel retailers across Australia structure tailored insurance solutions aligned with operational, environmental, cyber, and liability risks.

Important notice

This article is of a general nature only and does not take into account your specific objectives, financial situation or needs. It is also not financial advice, nor complete, so please discuss the full details with your insurance broker as to whether these types of insurance are appropriate for you. Deductibles, exclusions and limits apply. You should consider any relevant Target Market Determination and Product Disclosure Statement in deciding whether to buy or renew these types of insurance. Various insurers issue these types of insurance and cover can differ between insurers.

This article provides information rather than financial product or other advice. The content of this article, including any information contained in it, has been prepared without taking into account your objectives, financial situation or needs. You should consider the appropriateness of the information, taking these matters into account, before you act on any information. In particular, you should review the product disclosure statement for any product that the information relates to it before acquiring the product.

Information is current as at the date the article is written as specified within it but is subject to change. Global Insurance Solutions Pty Ltd make no representation as to the accuracy or completeness of the information. Various third parties have contributed to the production of this content. All information is subject to copyright and may not be reproduced without the prior written consent of Global Insurance Solutions Pty Ltd.

Risk Advisor, Insurance Broker & Director

With around 15 years in insurance, Yuvi Singh is a passionate Risk Advisor, Director, and Insurance Broker at Global Insurance Solutions. Backed by a Commerce degree and ANZIIF diploma, Yuvi leads a team servicing SMEs across industries like manufacturing, logistics, fuel, IT, and more. At GIS, clients benefit from tailored, transparent advice, access to 150+ insurers, and end-to-end risk solutions. Recognised as a 2022 Insurance Magazine Rising Star and 2024 Top Insurance Broker by Insurance Business Australia, Yuvi delivers flexible, effective outcomes with integrity and innovation.