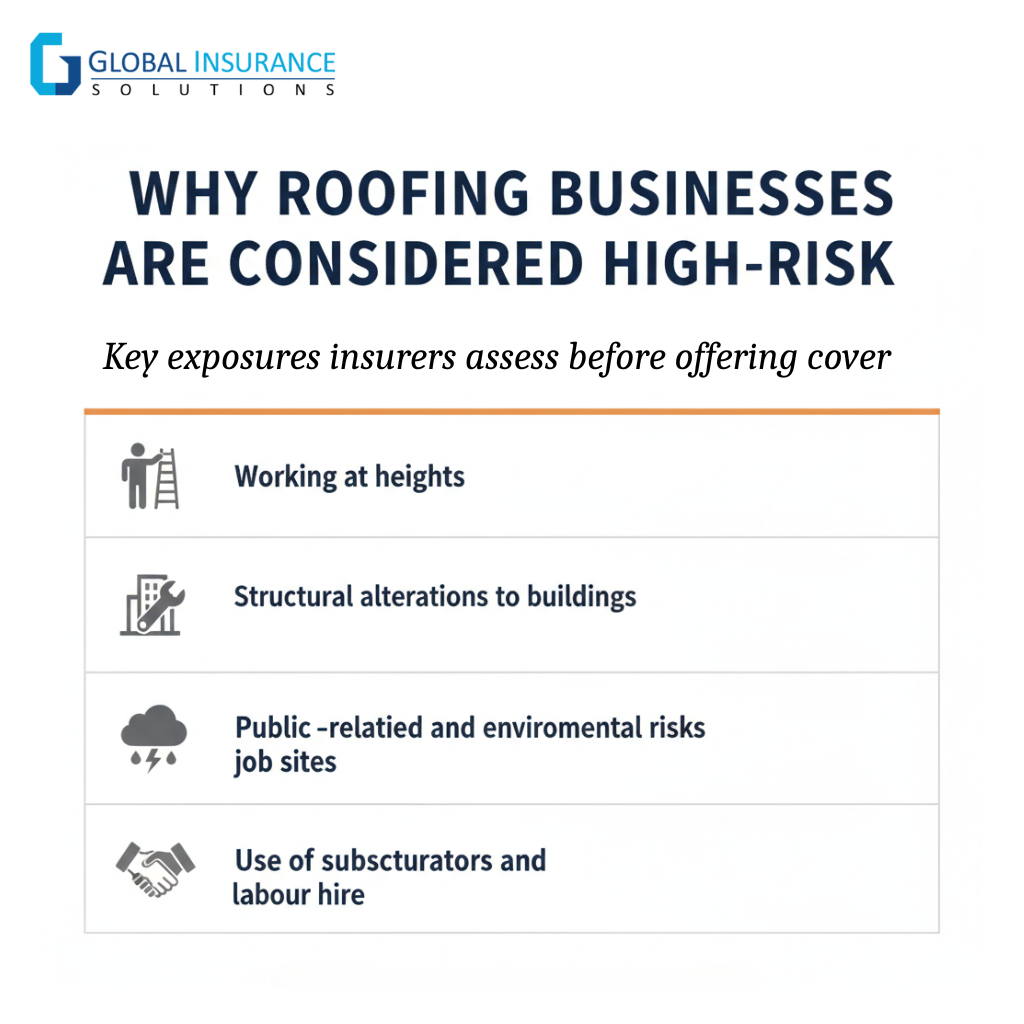

Roofers’ public liability insurance is the foundation of any roofing business insurance setup. It protects you if your work causes injury or property damage to a third party.

This includes:

- Falling materials injured a client

- Damage to neighbouring properties

- Water ingress caused by incomplete roofing work

- Injury to members of the public near the worksite

Most Australian builders, councils, and developers require public liability for roofers as a minimum contract condition.

Residential roofing insurance is designed for roofers working on homes, units, and townhouses.

Common risks include:

- Damage to internal ceilings and contents

- Injury to occupants

- Weather exposure during roof replacement

- Faulty flashing or tile installation

Residential work often involves a high frequency of claims, even if the claim values are relatively small.

Commercial roofing insurance applies to larger buildings, such as: Warehouses, Factories, Shopping centres, and Office buildings.

Commercial jobs typically involve:

- Higher contract values

- Longer project durations

- More complex liability chains

This is where commercial roofing contractor insurance becomes critical, especially when principal contractors push risk downstream.

Metal roofing insurance is essential because of the unique risks involved in this type of work, including heat expansion that can affect roof performance, fixing failures, sharp material hazards, and potential issues with structural integrity that may lead to damage or injury claims. Claims often involve water ingress or detachment during extreme weather.

Tile roofing insurance is designed to address the specific risks associated with tiled roofs, including breakage during installation, incorrect load distribution, potential roof collapse, and leaks caused by displaced or damaged tiles. Tile roofs generate frequent damage claims, especially during repairs.

Roof repair insurance is critical for contractors who carry out emergency repairs, storm damage fixes, and insurance claim work, as these jobs often involve higher-risk conditions, tight timeframes, and greater exposure to liability claims. Short-term repairs still carry long-term liability exposure.

Roof replacement insurance covers full strip and replace projects where exposure increases due to:

- Temporary roof removal

- Weather damage during works

- Extended project timelines

Roofing maintenance insurance applies to:

- Ongoing service contracts

- Scheduled inspections

- Gutter and drainage maintenance

Maintenance work often triggers claims when pre-existing damage is uncovered.

Risk Advisor, Insurance Broker & Director

With around 15 years in insurance, Yuvi Singh is a passionate Risk Advisor, Director, and Insurance Broker at Global Insurance Solutions. Backed by a Commerce degree and ANZIIF diploma, Yuvi leads a team servicing SMEs across industries like manufacturing, logistics, fuel, IT, and more. At GIS, clients benefit from tailored, transparent advice, access to 150+ insurers, and end-to-end risk solutions. Recognised as a 2022 Insurance Magazine Rising Star and 2024 Top Insurance Broker by Insurance Business Australia, Yuvi delivers flexible, effective outcomes with integrity and innovation.